US Mortgage Underwriting Interview Questions & Answers PDF

Us Mortgage Underwriting Interview Questions And Answers Pdf serves as a vital resource for professionals stepping into underwriting roles, offering deep insight into the evaluation standards, risk assessment protocols, and documentation rigor that shape lending decisions. Preparing for such interviews demands more than memorization—it requires a nuanced understanding of the principles behind mortgage approval processes, from income verification to credit history analysis. This comprehensive guide unpacks the most common questions, delivers clear answers, and provides practical context so candidates can confidently demonstrate their expertise in real-world scenarios.

Understanding the Core of Mortgage Underwriting Through Key Interview Questions

The interview process for mortgage underwriters centers on assessing creditworthiness, financial stability, and risk exposure. Candidates must articulate how they evaluate applicants’ income streams, debt-to-income ratios, employment history, and asset liquidity. Equally critical is knowledge of regulatory requirements like Dodd-Frank and guidelines from GSE agencies such as Fannie Mae and Freddie Mac. The Us Mortgage Underwriting Interview Questions And Answers Pdf serves not just as a Q&A tool but as a roadmap to mastering these interwoven concepts. Interviewers often probe how candidates distinguish between reliable income sources versus speculative earnings. For example: “How do you verify consistent income for a self-employed applicant?” The expected answer goes beyond checking W-2s—understanding documented business revenue, tax returns over three years, and industry stability adds depth. Similarly, questions about debt obligations explore total monthly payments relative to gross monthly income. A candidate might explain calculating DTI by adding all recurring debts—including car loans and student loans—and comparing them against stable gross earnings before mortgage application submission. Credit history remains a cornerstone inquiry. “What red flags do you look for in a credit report?” typically receives detailed guidance: prolonged late payments, high credit utilization exceeding 30%, or recent bankruptcies signal elevated risk. A strong answer contextualizes this within underwriting policy—some lenders tolerate one minor 30-day late entry if overall file strength is high; others flag it immediately. Understanding these nuances transforms generic knowledge into actionable judgment during interviews.

Documentation Standards: What Examinators Really Expect

A pivotal part of the Us Mortgage Underwriting Interview Questions And Answers Pdf addresses documentation rigor. Examiners assess whether candidates recognize original documents—such as pay stubs with employer stamps or notarized bank statements—must be authentic and current. Vague references to “original paperwork” fall short; instead, candidates should specify acceptable formats: scanned copies with clear dates and signatures or physical documents stored in secure folders with chain-of-custody notes. This precision reflects professionalism and adherence to compliance standards like RESPA and TILA-RESPA rules. Mortgage underwriters also emphasize data accuracy over completeness alone. An interview question may ask: “How do you handle discrepancies between reported income and bank records?” The best responses explain immediate verification steps—cross-referencing W-2s with past tax filings (Form 1040), confirming employer contact via phone or HR verification tools—and documenting findings transparently in the file rather than ignoring inconsistencies silently. This practice safeguards against future audits or loan defaults driven by misreported data. Employers often assess cultural fit through behavioral questions tied to teamwork and ethical judgment: “Tell us about a time you flagged irregularities during underwriting.” Here, candidates benefit from citing specific examples—like identifying an unusual property valuation discrepancy on appraisal documents—and describing how they escalated concerns through proper channels while maintaining confidentiality under BOC regulations. Such answers reveal not just technical skill but integrity under pressure—qualities underwriters value deeply in team-driven environments.

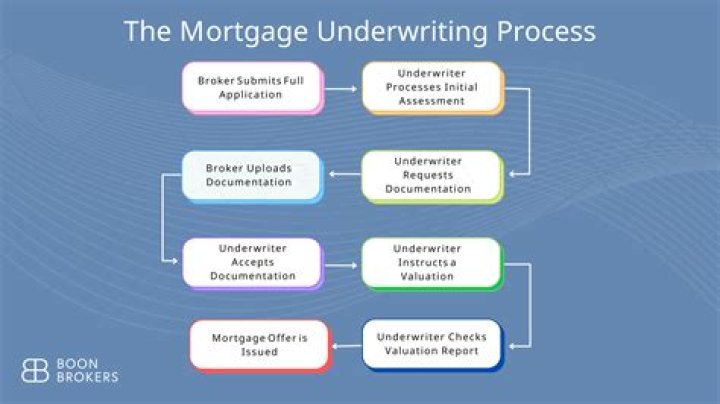

The Strategic Value of Practicing With Realistic PDF Resources

Accessing the Us Mortgage Underwriting Interview Questions And Answers Pdf offers more than repetition—it cultivates strategic clarity under pressure. These PDF materials are structured to simulate actual exam conditions: questions follow progressive complexity from foundational definitions (e.g., “What constitutes qualifying debt?”) to advanced scenarios involving mixed-income households or secondary mortgages with unique risk profiles. Regular review reinforces memory retention while sharpening analytical thinking across diverse case studies found within the document’s well-organized chapters. Moreover, many PDFs integrate visual aids—flowcharts mapping approval thresholds or tables summarizing credit score impacts—which support faster comprehension during interviews when quick yet accurate decisions are critical. Candidates who engage deeply with these tools develop sharper recall patterns; they learn not only what to say but how to frame responses using standardized terminology expected by lenders nationwide. This alignment boosts confidence exponentially when faced with unscripted follow-ups that test real-world judgment rather than rote knowledge alone. Ultimately, mastering this interview content equips future underwriters with both technical competence and emotional intelligence—the dual pillars demanded by modern lending standards where compliance intersects human insight every step of the loan lifecycle. In closing, Us Mortgage Underwriting Interview Questions And Answers Pdf isn’t merely a study guide—it’s a strategic bridge connecting academic preparation to frontline decision-making excellence in mortgage lending operations today’s dynamic financial landscape requires no less precision or professionalism from its practitioners.The path from theory to application begins here.