Testing Assumptions in Multiple Regression: A 4.5-Step PDF Guide

Understanding the 4.5. testing the assumption for multiple regression pdf is essential for anyone navigating the complexities of predictive modeling and statistical inference. This structured approach breaks down key assumptions, enabling researchers and analysts to validate their models with confidence and precision.

Navigating Critical Assumptions in Multiple Regression Through a Comprehensive PDF

In any multivariate analysis, multiple regression stands as a powerful tool—but only when its foundational assumptions hold true. The 4.5. testing the assumption for multiple regression pdf serves as a trusted roadmap, guiding practitioners through essential checks that prevent misleading conclusions and enhance model reliability.

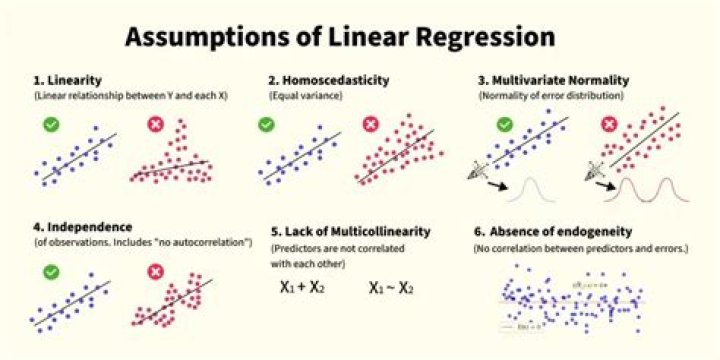

Multiple regression models rest on five core assumptions: linearity, independence of errors, homoscedasticity, normality of residuals, and absence of multicollinearity. Verifying these is not optional—it’s a necessity for valid inference. A well-structured PDF document transforms this daunting task into a manageable workflow, offering clear steps, visual cues, and practical examples.

First, verifying linearity ensures that relationships between predictors and the response variable are approximately linear across the range of observed data. Scatterplots with fitted lines help identify nonlinear patterns that could distort predictions. Next, independence requires that residuals are uncorrelated—drawn from Durbin-Watson tests or residual plots—to rule out autocorrelation in time-series contexts.

Homoscedasticity checks whether error variance remains constant across predictor values. Residual vs.fitted value plots expose funnel shapes signaling heteroscedasticity—common yet dangerous violations. Normality assumes residuals follow a Gaussian distribution; Q-Q plots and histograms expose skewness or heavy tails that threaten inference accuracy.

Perhaps most critical is assessing multicollinearity among independent variables. High pairwise correlations inflate standard errors, weakening significance tests. Variance Inflation Factor (VIF) thresholds—typically below 5 or 10—signal problematic redundancy requiring mitigation via variable removal or regularization.

A detailed PDF guide organizes these steps into digestible sections: diagnostic checks with recommended software commands (like R’s `vif()` or Python’s `statsmodels`), annotated visualizations highlighting red flags, and interpretation tips tailored to common pitfalls. This methodical structure supports both novices learning fundamentals and experts refining advanced applications.

Beyond technical rigor, the 4.5. testing the assumption for multiple regression pdf fosters analytical discipline—encouraging skepticism toward model outputs while empowering confident decision-making grounded in evidence. Each assumption checked strengthens trust in predictions used across fields from economics to engineering.

Ultimately, mastering these principles through structured documentation ensures robust modeling practices that withstand scrutiny and deliver actionable insights—proving indispensable in data-driven environments where accuracy demands precision.