Complete List of Liabilities in Accounting PDF

List Of Liabilities In Accounting PDF serves as a foundational document for understanding how obligations shape financial reporting and decision-making. This comprehensive guide explores every facet of liabilities, offering clarity on types, recognition rules, and practical implications in professional accounting. Whether you're managing books or auditing statements, mastering this list ensures accuracy and compliance.

The Core Elements of a List Of Liabilities in Accounting PDF

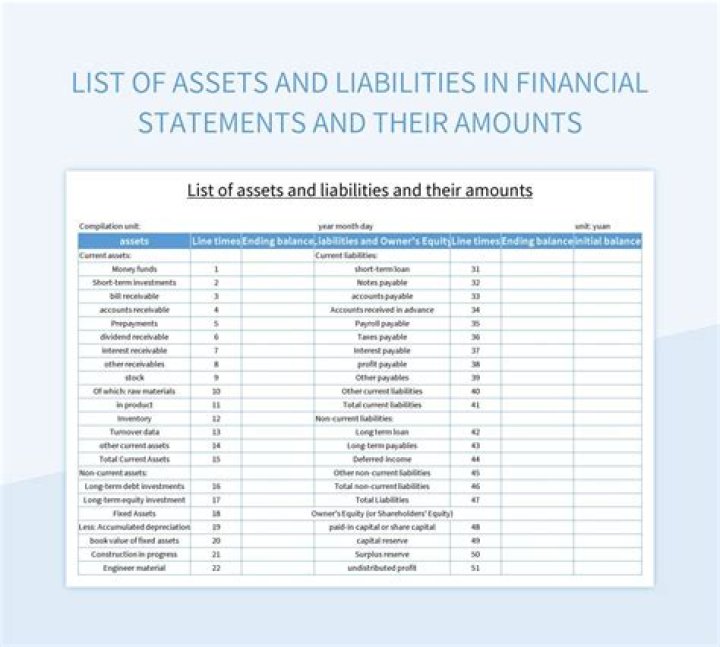

Understanding the structure and content of a List Of Liabilities In Accounting PDF is essential for accountants, auditors, and financial analysts. This document organizes financial responsibilities into clear categories, ensuring transparency in balance sheets and supporting sound fiscal management. Each liability reflects a probable future outflow, demanding careful assessment to uphold reporting integrity. The list typically begins with current liabilities—short-term obligations due within one year. These include accounts payable, accrued expenses, short-term loans, and unpaid taxes. Proper classification prevents misrepresentation of liquidity position. For example, deferring payment on supplier invoices stays current, while long-term debt conversion can distort near-term cash flow insights. Beyond current items lie non-current liabilities—longer-term commitments like bonds payable, leases outstanding beyond one year, pension obligations, and deferred tax liabilities. These require distinct accounting treatments under standards such as IFRS or GAAP. Recognizing their timing affects leverage ratios and solvency analysis significantly. Mismanaging these entries risks misleading stakeholders about the entity’s true financial health. Every liability entry must adhere to core accounting principles: probability of occurrence and measurable value. An estimate becomes necessary when precise amounts are uncertain—such as warranty claims or pending litigation settlements—but disclosures must remain transparent about assumptions used. Omitting key contingent liabilities breaches disclosure standards and invites regulatory scrutiny. Moreover, this List Of Liabilities In Accounting PDF supports internal controls by mapping exposures tied to specific departments or projects. Tracking segment-level obligations enhances risk assessment during audits or strategic planning sessions. Auditors verify these entries rigorously to confirm alignment with actual performance data and compliance with relevant frameworks like IFRS 9 or ASC 480 for financial instruments classification. In practice, preparing this document demands meticulous reconciliation of journals, adjusting entries, and intercompany reconciliations where applicable. Automation tools streamline calculations but human oversight remains critical to detect anomalies such as duplicate postings or mismatched maturities that software might overlook silently. Ultimately, the List Of Liabilities In Accounting PDF is more than a static record—it’s a dynamic financial narrative reflecting past decisions while informing future strategy through quantified risk exposure and capital structure insights.