Johansen Cointegration Test PDF: Step-by-Step Guide & Analysis

Johansen Cointegration Test PDF serves as an essential resource for economists and researchers analyzing long-term equilibrium relationships between non-stationary time series. This powerful statistical tool enables the detection of cointegration—patterns where multiple variables drift together over time despite short-term fluctuations. The Johansen Cointegration Test PDF provides a complete framework, combining theoretical rigor with practical guidance, making it indispensable in econometric analysis across fields like finance, macroeconomics, and environmental studies.

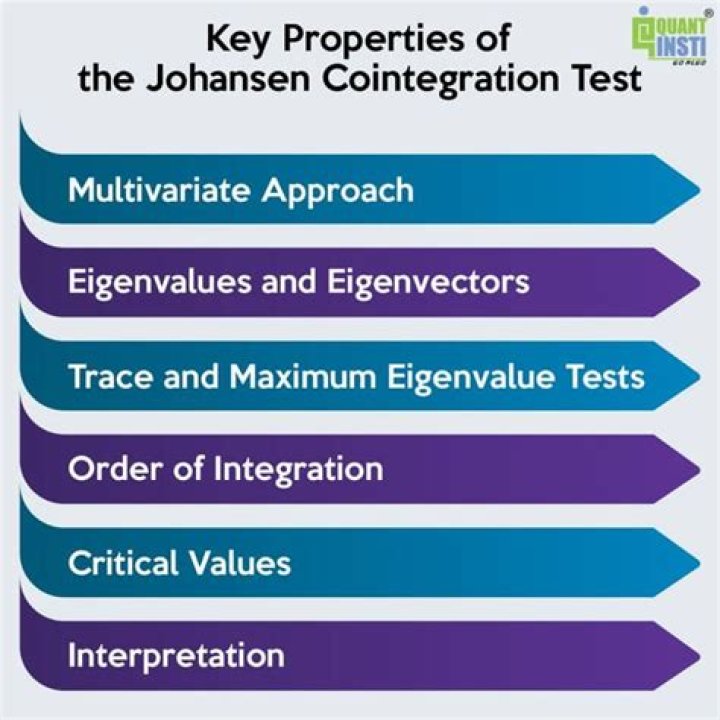

The Core Principles Behind Johansen Cointegration Test Pdf

Understanding Johansen Cointegration Test Pdf begins with grasping its theoretical foundation: if several time series share a common stochastic trend, they may be cointegrated—meaning a linear combination of them remains stationary. Unlike simpler tests such as Engle-Granger, the Johansen approach handles multiple variables efficiently through maximum likelihood estimation within a vector autoregressive (VAR) framework. The test identifies the number of cointegrating vectors, offering nuanced insights beyond mere detection—enabling deeper structural interpretation of dynamic systems.

The Johansen Cointegration Test PDF is structured to guide analysts through model specification, lag selection, and trace/stretch tests. It begins by establishing the VAR model order—critical for avoiding spurious results—and proceeds to estimate reduced-form equations. Each step is meticulously explained with mathematical clarity and practical intuition. Users learn how test statistics (such as trace and maximum eigenvalue) determine the presence and number of cointegrating relationships. This systematic flow ensures that even complex multivariate datasets become interpretable using well-documented procedures.

The PDF also integrates diagnostic checks—unit root tests, residual autocorrelation, and stability assessments—to validate model assumptions. These safeguards enhance reliability, allowing researchers to confidently apply findings in policy design or forecasting models. Whether analyzing GDP growth across countries or price movements in financial markets, the Johansen framework delivers robust insights grounded in statistical validity.

The availability of this test in PDF format transforms abstract econometric theory into actionable tools. Researchers can download it freely to replicate analyses or embed findings into larger research papers without losing methodological transparency. Each section balances formal derivation with accessible explanations, bridging academic depth and real-world applicability.

Johansen Cointegration Test Pdf stands out not only for its technical precision but also for its pedagogical structure. It demystifies advanced econometrics by walking readers through each analytical phase—from identifying stationarity challenges to final inference on long-term links between variables. This makes it an invaluable companion for both seasoned practitioners and students navigating multivariate time series analysis.

The importance of mastering this test lies in its ability to uncover hidden economic relationships masked by random walks or trends. When properly applied via the Johansen Cointegration Test Pdf resources, analysts reveal structural equilibria that inform better decision-making in uncertain environments. The widespread accessibility of this PDF empowers global scholarship, accelerating innovation across disciplines dependent on rigorous time series modeling.

Johansen Cointegration Test Pdf remains more than a statistical procedure—it embodies a pathway to deeper understanding of complex systems where variables evolve together over time. By combining theoretical depth with clear exposition, it equips users to extract meaningful patterns from noisy data.**