International Comparison of Strategic Management Accounting Practices PDF

An International Comparison Of Strategic Management Accounting Practices Pdf reveals how diverse economic systems and regulatory environments shape how organizations measure, analyze, and apply accounting information for strategic decision-making. This comparative lens exposes fundamental differences in methodologies, reporting standards, and the integration of financial data with long-term business goals across countries. From Japan’s consensus-driven approaches to the United States’ results-oriented frameworks, each nation reflects unique cultural, legal, and market influences on strategic accounting practices.

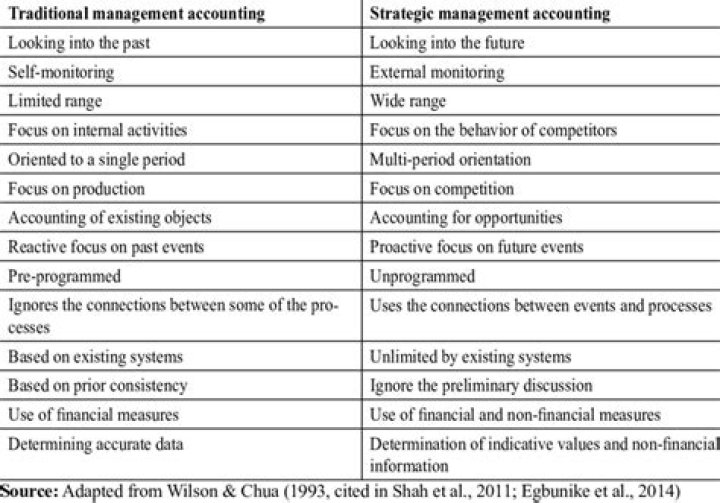

Global Foundations of Strategic Management Accounting

Strategic management accounting transcends traditional bookkeeping by embedding forward-looking financial analysis into corporate strategy. An International Comparison Of Strategic Management Accounting Practices Pdf highlights stark contrasts in how companies assess performance and allocate resources. In Europe, for instance, companies often emphasize balanced scorecards that integrate non-financial indicators—aligning operational metrics with sustainability targets. Meanwhile, emerging economies frequently adapt international standards like IFRS cautiously, adjusting disclosures to fit local governance norms and economic realities.

The role of audit transparency varies significantly: while Nordic countries enforce rigorous third-party reviews to enhance accountability, some Asian markets prioritize confidentiality within strategic planning circles. These differences influence stakeholder trust and long-term competitiveness. Understanding such variances helps multinational firms design adaptable accounting systems that meet both global expectations and regional demands.

Each nation’s approach to strategic management accounting mirrors deeper cultural values—whether collectivist consensus in East Asia or individualist innovation in North America—shaping how performance is measured and strategies are refined.

An International Comparison Of Strategic Management Accounting Practices Pdf serves as a critical resource for scholars and practitioners alike. It not only maps disparities but also identifies best practices transferable across borders. For example, German firms’ meticulous cost allocation models inspire precision in capital budgeting elsewhere, while Scandinavian emphasis on real-time data analytics pushes boundaries in predictive reporting.

The PDF format enables rich integration of tables, flowcharts, and comparative frameworks that illuminate nuanced differences often lost in textual summaries alone. Interactive charts track variance analysis trends; embedded case studies reveal real-world applications under varying regulatory regimes. This visual depth supports informed decision-making for organizations navigating cross-border operations.

The evolving convergence toward global standards coexists with persistent local adaptations—reflecting a dynamic balance between uniformity and contextual responsiveness.

Conclusion: An International Comparison Of Strategic Management Accounting Practices Pdf demonstrates that no single model fits all contexts. Instead, successful implementation requires blending global insights with localized execution—honoring cultural nuances while leveraging universal principles of transparency and strategic alignment. As markets grow more interconnected, this adaptive mindset becomes essential for sustainable competitive advantage.