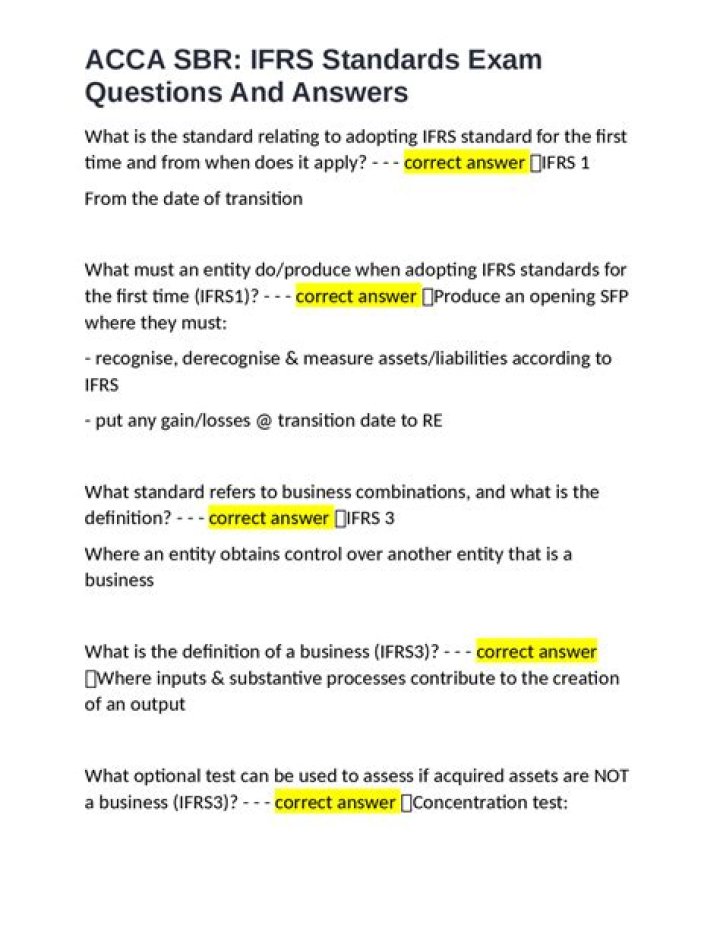

IFRS 3 Questions and Answers PDF – Expert Guide & Solutions

Ifrs 3 Questions And Answers Pdf remains a vital resource for finance professionals navigating the complexities of business combinations under international accounting standards. Understanding IFRS 3 is essential not only for compliance but also for accurate financial reporting and strategic decision-making. This guide explores common queries and delivers clear, reliable answers through a structured PDF format, making it easier to study and apply key principles.

Understanding the Core Principles of IFRS 3: Business Combinations

IFRS 3 Questions And Answers Pdf begins with a clear foundation in the standard’s core framework—recognizing and measuring business combinations. The standard mandates that when an entity acquires control over another, it must account for the acquisition as a combination, integrating identifiable assets, liabilities, and contingent considerations into a single unified measure. This shift from previous rules emphasizes fair value measurement as the cornerstone of reporting, ensuring transparency across global markets. The detailed Q&A section illuminates how to identify goodwill, non-controlling interests, and the treatment of acquisition-related costs—each critical to avoiding material misstatements.

Navigating common pitfalls is where this PDF proves indispensable. Many practitioners struggle with timing recognition or classifying intangible assets correctly. The expert answers clarify that only costs directly attributable to securing control qualify as acquisition costs—excluding general administrative expenses. Similarly, non-controlling interests are distinct from joint arrangements; they reflect the equity share held by minority owners post-acquisition. These nuances are unpacked with precision in the PDF, transforming confusion into clarity.

Step-by-Step Application of IFRS 3: From Identification to Presentation

The journey from identification to final financial presentation unfolds methodically through ifrs 3 questions and answers pdf. First, entities must identify the acquirer—the entity that obtains control—based on voting rights or contractual agreements. Once established, the net identifiable assets are measured at fair value: assets removed from the prior owner’s balance sheet are added, while liabilities are recorded at their true economic cost. Intangible assets like trademarks or customer relationships receive explicit valuation guidance, ensuring no opportunity for arbitrary impairment testing.

Subsequent steps involve recognizing goodwill—the excess of purchase price over fair value—and allocating it across acquired components based on relative fair values. The PDF addresses how post-acquisition adjustments impact this figure, including remeasurements under subsequent events. Each scenario is grounded in practical examples: whether it’s a merger involving multiple legal entities or an asset purchase with deferred consideration. These real-world illustrations reinforce learning and prepare users for audits and stakeholder communications.

Even complex topics like contingent consideration receive thorough coverage. Payments tied to future performance require careful assessment—are they probable? Measurable? The ifrs 3 questions and answers pdf breaks down evaluation criteria and recognition thresholds clearly, helping practitioners avoid overvaluation or premature liability recording.

The Value of Structured Learning Through PDF Documentation

One of the strongest advantages highlighted in this guide is how structured PDF documentation transforms abstract standards into accessible knowledge tools. Unlike fragmented online snippets or verbose manuals, this document presents Ifrs 3 Questions And Answers Pdf as a cohesive learning companion—ideal for self-study or classroom use alike. The organized layout supports progressive mastery: starting with foundational definitions before advancing to transaction-specific rules and exception handling.

The inclusion of annotated examples strengthens retention; readers encounter not just theoretical frameworks but also how they apply under varying circumstances—such as partial acquisitions or cross-border combinations involving multiple jurisdictions. Each answer is crafted to anticipate common misinterpretations, preempting errors before they occur in practice.

The reliability of this resourcestems from its alignment with authoritative interpretations issued by standard-setting bodies like IASB. Regular updates ensure relevance amid evolving guidance or regulatory changes—critical in fast-moving financial environments where outdated practices risk non-compliance penalties. Ultimately, mastering IFRS 3 hinges on consistent engagement with precise educational materials—exactly what ifrs 3 questions and answers pdf delivers through disciplined structure and clarity. Whether preparing for certification exams or refining daily reporting processes, having this PDF as a reference empowers professionals to act confidently within strict accounting boundaries.

This expertly curated PDF stands not merely as an answer sheet but as a strategic tool fostering deeper comprehension—and confidence—in applying IFRS 3 standards across diverse business contexts.The power lies in preparation shaped by precision.