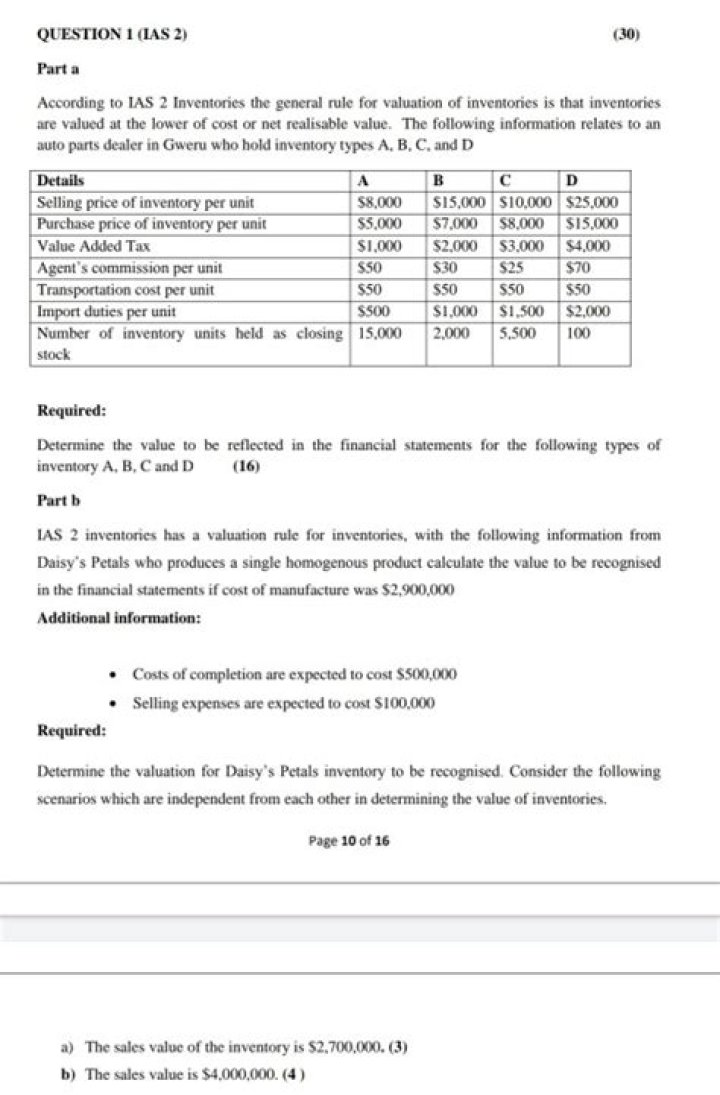

IAS 2 Inventories Q&A PDF: Key Questions & Answers

Ias 2 Inventories Q&A PDF contains essential insights for understanding asset valuation, recognition, and reporting under International Accounting Standard 2, forming a vital resource for professionals navigating complex inventory accounting standards. Mastering the concepts within this PDF empowers users to answer critical questions with confidence and precision.

Mastering IAS 2: Core Questions and Answers in Inventory Accounting

IAS 2 Inventories Questions And Answers Pdf serves as a cornerstone for accounting practitioners dealing with asset measurement and classification. This framework guides the treatment of inventories from acquisition to disposal, ensuring compliance with global reporting standards. Exploring common queries helps clarify ambiguities that often arise in practice.

Understanding inventory valuation methods under IAS 2 demands clarity on cost models—whether FIFO, weighted average, or specific identification—and how these influence financial statements. A frequently asked question centers on when inventory should be measured at historical cost versus net realizable value, especially during periods of market volatility. The standard permits revaluation only in limited circumstances, reinforcing the importance of consistent application.

Another pivotal area involves identifying obsolescence risks and impairment losses. The PDF often highlights scenarios where inventory becomes impaired due to declining market demand or technological changes. Professionals must assess whether carrying amounts exceed recoverable amounts, triggering write-downs that reflect economic reality.

The Q&A document also addresses inventory write-downs during business combinations and amortization of intangible assets linked to stock systems. These topics underscore the interconnectedness of inventory management with broader financial reporting principles.

The structured format of IAS 2 Inventories Questions And Answers Pdf enables efficient learning and quick reference. Key points include: - Inventories must be measured at the lower of cost or net realizable value; - Costs include purchases, handling, and conversion expenses; - Reversals of prior write-downs are generally prohibited; - Inventory impairments require systematic testing for recoverability; - Proper documentation supports audit readiness.

This comprehensive guide simplifies complex rules into actionable guidance. By studying this PDF, professionals gain confidence in applying standards during audits or internal reviews.

In conclusion, IAS 2 Inventories Q&A PDF stands as an indispensable tool for accurately capturing inventory values under international standards. Its role extends beyond compliance—it fosters transparency and reliability in financial reporting, helping organizations make informed operational decisions grounded in sound accounting principles.