Home Loan Documents List PDF: Everything You Need for Applying

Home Loan Documents List PDF serves as a foundational blueprint for borrowers navigating the complex journey of securing a mortgage. Whether you’re a first-time homebuyer or experienced in real estate financing, understanding which documents are required ensures a smooth application process and avoids costly delays. This comprehensive guide unravels the essential paperwork, offering clarity on what to gather, why each item matters, and how to present them effectively—all laid out in a clear Home Loan Documents List PDF format.

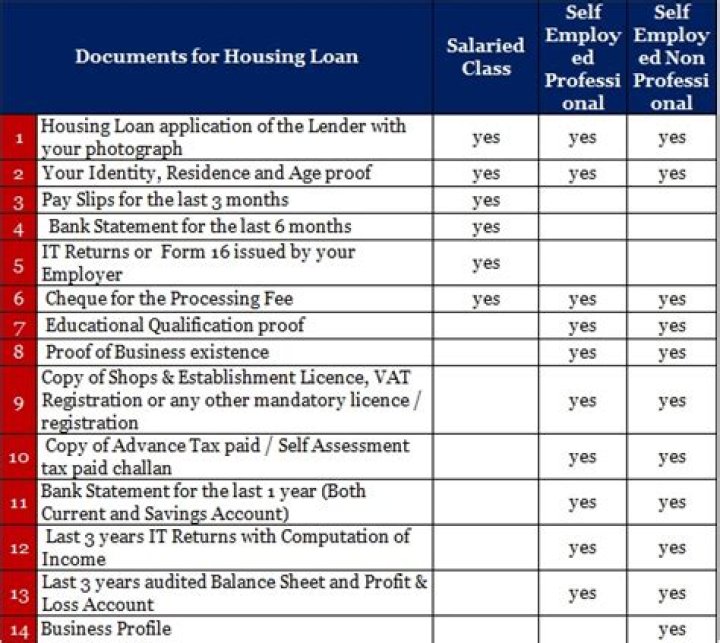

The Essential Components of a Home Loan Documents List PDF

To successfully apply for a home loan, lenders require detailed proof of identity, income, employment, and financial stability. A Home Loan Documents List PDF organizes these critical elements into a structured checklist that streamlines submission and verification. Without this document set, even strong credit profiles can face rejection due to incomplete paperwork. Preparing this list early not only accelerates approval but also builds confidence by reducing uncertainty. At the heart of any Home Loan Documents List PDF are identity verification materials—passport or driver’s license and social security card. These documents confirm your legal identity and residency status, forming the first checkpoint for lenders. Without valid photo ID and national identification records, verifying your status becomes significantly more difficult. Lenders rely heavily on these papers to prevent fraud and ensure regulatory compliance throughout the lending cycle. Proof of income follows closely as a cornerstone document. Pay stubs from current employers, tax returns (especially for self-employed applicants), and recent bank statements collectively demonstrate financial capacity to repay the loan. These sources show consistent earnings patterns and help lenders assess debt-to-income ratios with precision. The inclusion of multiple income streams—such as freelance work or passive investments—can strengthen your application by illustrating stability beyond primary employment. Employment verification is equally vital; recent letters from supervisors detailing job roles and tenure add credibility to income claims. For salaried individuals, pay stubs spanning the last two months offer concrete evidence of steady paychecks over time. Self-employed borrowers must go further—providing profit-and-loss statements alongside contract records ensures transparency about business-generated revenue tied to home financing goals. Credit history forms another pillar of any reliable Home Loan Documents List PDF. Lenders scrutinize credit reports to evaluate repayment behavior over years past—payment timeliness, existing debt obligations, and outstanding balances all influence loan terms like interest rates and down payment requirements. Recent credit inquiries may also appear here; while some are routine during application checks, excessive recent checks can raise red flags about financial stress or overextension. Collateral documentation rounds out this essential collection—property deeds proving ownership or mortgage eligibility confirms asset backing that secures the loan against default risk. For renters seeking purchase assistance programs, lease agreements or rent payment histories may substitute temporarily but still serve as proof of stable living arrangements essential for qualifying finance offers. Finally, supplementary materials such as bank statements verify liquidity reserves needed for down payments or closing costs—a practical demonstration that funds exist beyond regular income flows. Though not always mandatory across all lenders, including these records showcases financial responsibility critical in tightening credit environments where conservative underwriting prevails. In summary, maintaining a complete Home Loan Documents List PDF transforms an intimidating loan process into a manageable checklist grounded in preparation and transparency. Each document plays a strategic role in validating eligibility while reflecting personal financial maturity—ultimately shaping approval likelihood and long-term borrowing terms with clarity rooted in real-world evidence rather than guesswork alone.