Calculate Credit Score Impact on Loan Approval Answers

Calculate Impact Of Credit Score On Loans Answer Key Pdf reveals critical insights into how credit scores shape lending outcomes. Lenders rely on this data to assess risk and determine loan eligibility, making understanding the connection essential for borrowers and financial professionals alike. A detailed analysis uncovers patterns in approval rates, interest charges, and loan terms tied directly to credit history. This guide explores the mechanics behind these calculations, highlighting why credit scores carry such weight in loan decisions.

The Mechanics Behind Credit Score Evaluation

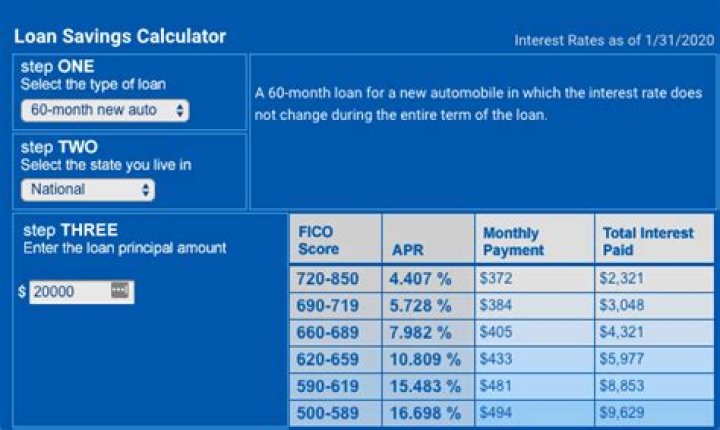

Credit scoring models, such as FICO and VantageScore, assign numerical values based on payment history, debt levels, credit age, new credit inquiries, and credit mix. Each factor influences the score differently. For example, consistent on-time payments boost the score significantly—often boosting approval odds. Meanwhile, high utilization of available credit strains it, leading to lower scores and higher borrowing costs. The answer key PDF documents precise thresholds where small score changes trigger major shifts in loan terms.

When evaluating loan applications, lenders cross-reference these scores with underwriting guidelines embedded in the answer key. A score above 740 typically signals strong creditworthiness; applicants often qualify for lower interest rates and favorable repayment periods. Scores between 670 and 739 suggest moderate risk—approval is likely but with stricter terms or higher rates. Below 670 marks a zone of caution: many lenders may deny or demand larger down payments to offset perceived risk.

Calculate Impact Of Credit Score On Loans Answer Key Pdfacts as a benchmark for both applicants seeking clarity and advisors preparing clients for real-world outcomes. The document outlines specific scenarios: how a 100-point increase can reduce interest rates by hundreds of dollars annually over a 30-year mortgage. It also explains variance—why two borrowers with similar incomes might receive different offers based solely on their scores.

Beyond interest rates, this PDF clarifies how lenders gauge risk through scoring tiers. A poor score below 600 often results in outright denial or alternative financing with exorbitant fees. Even modest improvements can unlock better options—turning financial barriers into manageable pathways. Lenders’ internal logic mirrors broader economic principles: minimizing default probability while maximizing portfolio profitability through data-driven decisions.

The answer key’s structure itself matters—it organizes variables logically: payment behavior first (most influential), followed by debt-to-income ratios and account history. Understanding this hierarchy empowers borrowers to prioritize actions that yield maximum benefit during applications.In conclusion, Calculate Impact Of Credit Score On Loans Answer Key Pdf is more than a reference—it’s a strategic tool that demystifies lending algorithms. By mastering its logic, borrowers gain leverage; advisors deliver precision. This knowledge transforms abstract numbers into actionable insight—turning uncertainty into informed opportunity.