Auditing Management Assertions PDF Guide

Auditing Management Assertions.pdf stands as a cornerstone document for professionals navigating the complex terrain of internal controls and financial reporting. This comprehensive guide enables auditors to evaluate the integrity of management assertions embedded within financial records, ensuring accuracy, completeness, and compliance. By systematically examining key assertions—such as existence, completeness, valuation, and cutoff—auditors gain critical insights into potential misstatements and risks. Understanding how to interpret and apply the findings from Auditing Management Assertions.pdf transforms routine checks into strategic assessments that strengthen organizational accountability and transparency.

Understanding Auditing Management Assertions PDF

Auditing Management Assertions.pdf serves as a vital reference in modern auditing practices, bridging theoretical frameworks with practical application. It consolidates core principles that auditors rely on to verify that financial statements reflect true economic conditions. These assertions are not mere checklists but dynamic tools for evaluating management’s reliability in presenting financial data. When reviewed systematically, the PDF reveals patterns in control effectiveness, uncovering weaknesses before they escalate into material errors or fraud.

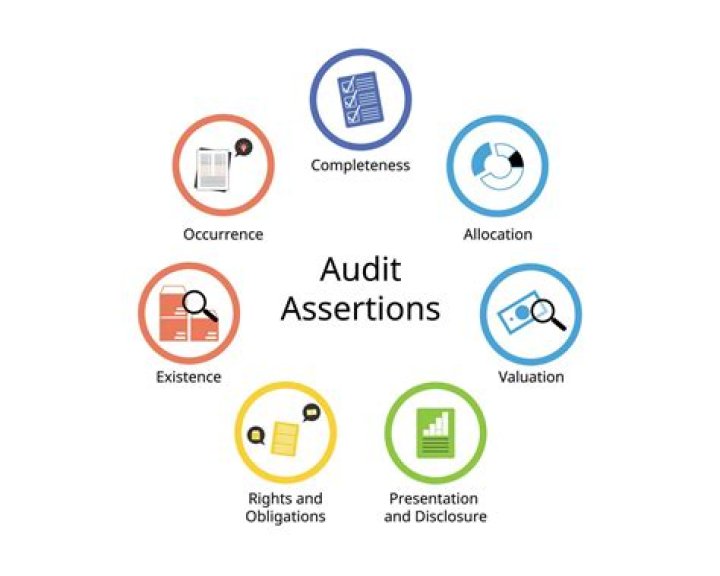

The structure of Auditing Management Assertions.pdf is deliberately designed to guide auditors through each assertion with clarity. It begins by defining fundamental concepts—existence confirms assets and liabilities actually exist; completeness checks for omitted items; valuation ensures values are recorded accurately; rights and obligations highlight legal ownership; and cutoff verifies transactions are recorded in the correct period. Each element demands careful scrutiny, supported by detailed examples that illustrate how misinterpretations can lead to significant audit findings.

Auditing Management Assertions.pdf also emphasizes the importance of professional skepticism. It teaches auditors to question inconsistencies, probe unusual transactions, and validate supporting documentation rigorously. By integrating this mindset with structured assessment techniques from the PDF, auditors enhance their ability to detect anomalies early. This proactive approach not only improves audit quality but also reinforces stakeholder confidence in financial reporting integrity.

In practice, using Auditing Management Assertions.pdf requires more than passive reading—it demands active engagement. Auditors must map organizational processes against assertion criteria, document observations meticulously, and communicate findings clearly to management and oversight bodies. The PDF acts as both compass and checklist, enabling a balanced mix of judgment and evidence-based analysis that aligns with global auditing standards.

Ultimately, mastering Auditing Management Assertions.pdf empowers professionals to elevate their audit effectiveness beyond technical compliance into strategic risk management. It transforms financial verification from a mechanical task into a thoughtful examination of control environments and human judgment—critical components in safeguarding organizational health and public trust.