How to Test Goodwill Impairment Under AICPA Guidelines: A Detailed Accounting & Valuation Guide (PDF)

Aicpa Accounting And Valuation Guide Testing Goodwill For Impairment Pdf is an essential resource for finance professionals navigating the complexities of goodwill impairment assessment under established accounting standards. This comprehensive PDF guide clarifies critical procedures, ensuring compliance and accuracy in evaluating whether goodwill assets remain properly valued on financial statements.

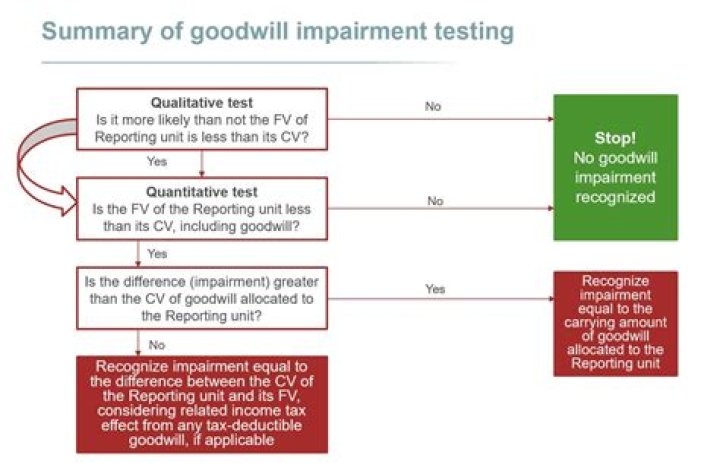

Understanding the Core Principles of Goodwill Impairment Testing Under AICPA Standards

Goodwill, often arising from acquisitions, represents more than just brand value or customer loyalty—it reflects intangible synergies that must be rigorously tested for impairment. The Aicpa Accounting And Valuation Guide Testing Goodwill For Impairment Pdf outlines a structured framework for assessing whether the carrying value of goodwill exceeds its recoverable amount. This process hinges on two key steps: first, estimating future cash flows attributable to the goodwill-bearing unit, and second, comparing these estimates to the current book value. If the carrying value surpasses recoverable amounts, an impairment loss must be recorded immediately. The AICPA guidelines emphasize consistency and transparency, demanding clear documentation at every stage. Unlike simplistic tests that ignore market dynamics or future expectations, this guide requires careful consideration of discounted cash flow models and scenario analyses. Professionals using this PDF gain insight into how assumptions about growth rates, discount factors, and residual values directly influence impairment outcomes—making strategic judgment as vital as technical precision.

The methodology detailed in the Aicpa Accounting And Valuation Guide Testing Goodwill For Impairment Pdf transforms abstract accounting rules into actionable steps. It begins with identifying reporting units where goodwill is held—often post-acquisition business segments—and proceeds to validate whether external factors or internal performance metrics justify a reassessment. Valuation techniques such as excess earnings models or market comparables are contextualized within practical applications, helping practitioners avoid common pitfalls like overreliance on historical data or flawed forecasting assumptions. Equally important is understanding timing: impairment testing isn’t a one-time event but part of ongoing monitoring. The guide stresses periodic reviews aligned with business changes—such as restructuring or shifts in market conditions—to ensure timely recognition of value declines before financial statements become misstated. This proactive stance safeguards both investor confidence and regulatory compliance in an environment where asset misvaluation carries significant legal and reputational risks.

By integrating detailed calculations with real-world examples, the Aicpa Accounting And Valuation Guide Testing Goodwill For Impairment Pdf bridges theory and practice seamlessly. It equips accountants and financial analysts with tools to assess impairment under varying scenarios—from stable operations to abrupt downturns—ensuring decisions reflect both quantitative rigor and qualitative judgment. Whether preparing for audits or internal controls review, mastering these steps empowers organizations to uphold integrity in financial reporting while adapting swiftly to evolving economic landscapes.

Ultimately, this PDF serves not only as a compliance manual but as a strategic roadmap for managing intangible assets wisely. It reinforces that sound goodwill impairment testing balances precision with practicality—critical for maintaining accurate balance sheets and supporting long-term financial stability.