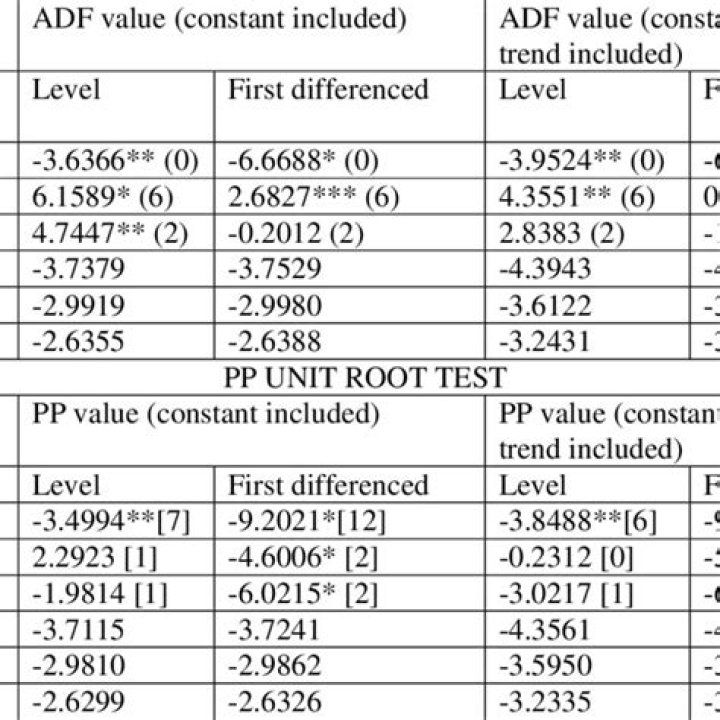

ADF Unit Root Test PDF: How to Check Stationarity & Avoid Spurious Regression

Understanding whether a time series is stationary is crucial before building predictive models—this is where the ADF Unit Root Test PDF becomes an essential tool. Adf Unit Root Test Pdf provides a structured way to assess stationarity, helping analysts avoid misleading results from spurious regressions that plague economic and financial data. By leveraging this test, researchers and practitioners can validate the stability of trends, seasonality, and underlying patterns in real-world datasets.

The Importance of Stationarity in Time Series Analysis

Adf Unit Root Test Pdf serves as a statistical gateway to determine if a time series possesses a unit root—an indicator of non-stationarity. When data exhibits a unit root, mean reversion fails, leading to unstable variance over time. This instability distorts correlations and inflates regression coefficients, rendering standard inferences unreliable. In fields like economics, finance, and climate science, where time-dependent data dominate, failing to detect non-stationarity risks constructing models built on fragile foundations. The ADF test offers clarity by testing the null hypothesis that a series contains a unit root against the alternative of stationarity.

The ADF test comes in multiple forms—Augmented Dickey-Fuller being the most common—each designed to account for autocorrelation in lagged values. Unlike simpler tests such as the Dickey-Fuller test, it adjusts for higher-order autoregressive processes by including lagged differences of the variable. This adjustment improves power and reliability when analyzing complex datasets with memory effects. The resulting p-value from an ADF Unit Root Test PDF directly informs model selection: a low p-value below 0.05 typically supports stationarity, justifying traditional regression approaches.

Interpreting output from an ADF test requires careful attention to both statistical significance and context. A rejection of the null hypothesis suggests stationarity; however, near-rejection regions demand skepticism—data may appear stable but still harbor structural breaks or nonlinear trends invisible to basic tests. Graphical analysis alongside the test result enhances confidence: plotting series with rolling means or differencing helps confirm whether deterministic or stochastic processes govern behavior. Moreover, seasonal patterns or abrupt regime shifts can mask unit roots if unaddressed.

Generating an Adf Unit Root Test PDF need not be complex; dedicated statistical software packages such as Stata, R (with `ur.test()`), Python (`statsmodels`), and MATLAB offer built-in functions producing comprehensive reports. These outputs include test statistics, adjusted p-values, critical values for different lag specifications, and diagnostic checks for serial correlation in residuals via Ljung-Box tests. Including these elements ensures transparency and facilitates peer review.

A key caveat lies in data preparation: missing values must be handled rigorously before testing to prevent biased outcomes. Additionally, integrating structural break tests—like those embedded in some extended ADF variants—strengthens robustness when dealing with policy shifts or external shocks common in macroeconomic data. Ignoring such factors risks false conclusions about stationarity.

The practical value of Adf Unit Root Test Pdf extends beyond theoretical validation—it empowers decision-makers across sectors to build resilient models grounded in sound statistical principles. From forecasting GDP growth to analyzing asset price movements, ensuring stationarity prevents erroneous forecasts fueled by spurious relationships. As datasets grow larger and more intricate, mastering this test becomes indispensable for credible quantitative research.

In conclusion, the Adf Unit Root Test PDF remains a cornerstone technique for diagnosing stationarity in time series analysis. Its proper application safeguards against misleading inferences while illuminating true dynamics hidden beneath noisy observations. Whether using manual calculations or automated software tools, this method bridges theory and practice—ensuring models reflect reality rather than artifacts of non-stationary behavior.