150 Accounting Interview Questions And Answers Pdf

Mastering the 150 Essential Accounting Interview Questions and Answers PDF

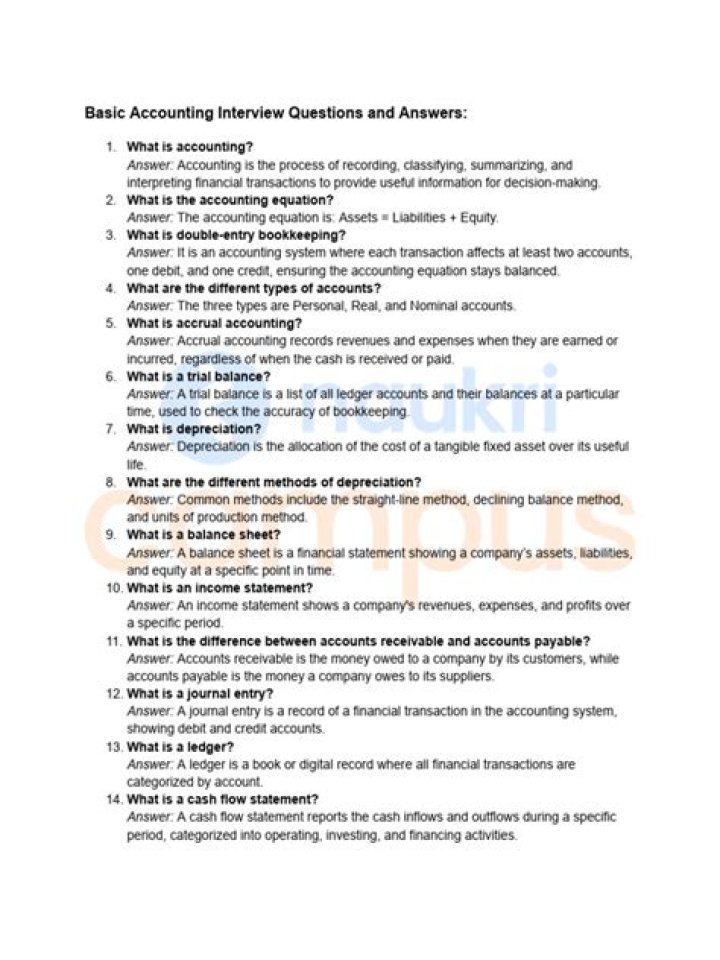

Preparing for an accounting interview demands thorough knowledge of core principles, practical skills, and real-world application. A key resource that transforms confidence into competence is a well-structured 150 Accounting Interview Questions and Answers PDF—your guide to mastering every concept from financial reporting to tax compliance. This comprehensive compilation bridges theory and practice, helping candidates articulate insights clearly while demonstrating technical expertise under pressure. Whether you're a student or a seasoned professional stepping into new roles, this PDF delivers structured clarity across all essential domains.

The Foundation: Core Financial Reporting Concepts At the heart of accounting lies financial reporting, where accuracy defines success. A typical starting point in any 150 Accounting Interview Questions And Answers PDF is the principles behind balance sheets and income statements. Candidates must explain how assets are recognized, liabilities classified, and revenues matched with expenses—highlighting concepts like accrual accounting and materiality. Understanding GAAP and IFRS frameworks ensures alignment with global standards, a critical area many interviewers probe deeply. For example: How does revenue recognition affect financial statements? The answer centers on performance obligations and timing, showing awareness of ASC 606 or IFRS 15 depending on jurisdiction. Key questions probe deeper into cash flow analysis: Why is operating cash flow more telling than net income? Because it reveals actual liquidity beyond accruals. Similarly, distinguishing between fixed and current assets clarifies short-term solvency assessments—essential for stakeholders evaluating growth potential. Practical examples anchor answers: “If inventory exceeds $50k annually under IFRS, it must be valued at lower of cost or net realizable value,” demonstrates mastery in applying rules to real data. Another common thread explores internal controls: What safeguards prevent errors in financial reporting? Strong responses reference segregation of duties, regular reconciliations, automated validation tools, and audit trails—each reducing risk while supporting compliance with SOX or other regulations. Interviewers test not just knowledge but judgment: How would you handle a discrepancy in accounts payable? A robust answer outlines investigation steps—reviewing invoices, confirming vendor details—and escalation protocols to leadership when material variances arise. Taxation & Compliance: Navigating Legal Obligations Tax-related questions dominate interviews where accounting meets law. Expect to explain VAT/GST mechanics: How does input tax credit work across borders? Candidates must clarify timing differences between taxable events and accounting periods while avoiding double taxation through treaty provisions. Transfer pricing poses another challenge—how do multinational firms ensure arm’s length pricing? The answer highlights OECD guidelines and documentation rigor to withstand scrutiny from tax authorities. Employee benefit plans demand precision too: What distinguishes defined benefit from defined contribution schemes? Defined benefit commitments require actuarial valuations projecting future liabilities; employers must fund these obligations conservatively using discount rates aligned with market yields. Meanwhile, retirement plans like 401(k)s involve fiduciary duties—ensuring assets are managed prudently in line with plan documents—and accurate quarterly Form 5500 filings to maintain regulatory compliance. The role of digital tools is increasingly vital—can automation replace manual bookkeeping? While software streamlines data entry and reconciliation speedily, human oversight remains irreplaceable for interpreting exceptions or resolving complex journal entries that systems cannot auto-correct. Forensic & Managerial Accounting Insights Beyond basic booksmanship lie forensic investigations and strategic decision support. Forensic queries test analytical rigor: How detect fraud through unusual transaction patterns? Patterns include round-dollar payments outside cycle norms or vendor concentration without proper approval—red flags demanding deeper forensic audit workflows involving data analytics software like ACL or Tableau for anomaly detection. Managerial accounting challenges assess cost behavior understanding: Why do fixed costs remain constant despite production shifts? Candidates link this to production levels—fixed costs like rent scale with output capacity but not per-unit cost—critical for budgeting precision during variance analysis between planned vs actual results. Activity-based costing (ABC) further refines overhead allocation by identifying true drivers such as machine hours or order volume rather than simplistic volume metrics alone. Moreover, performance metrics require clarity on KPIs tied to profitability: Return on assets (ROA) measures efficiency by comparing net income to total assets; return on equity (ROE) evaluates investor returns via net profit divided by shareholder equity—both revealing strategic effectiveness across departments or product lines when benchmarked against industry standards. Technical Proficiency & Tools Usage Modern accountants rely heavily on technology platforms requiring hands-on familiarity embedded in any top 150 Accounting Interview Questions And Answers PDF: ER